“Cooperatives exist not because money is scarce, but because understanding is rare.”

Botswana has long celebrated the idea of community. From shared water wells to local savings groups, our collective spirit is woven into the fabric of society. Nowhere is this more visible than in our cooperatives. These institutions, often small, sometimes fragile, are a lifeline for communities where formal banks hesitate to tread. They are meant to be engines of inclusion, trust, and shared prosperity.

And yet, time and again, they falter. They collapse, disband, or quietly sputter along, leaving behind disappointed members and the faint echo of lost promise. It is tempting to dismiss these failures as unfortunate, as a simple consequence of human error. But the truth is deeper, more structural, and far more revealing about the state of finance and governance in Botswana.

“In every community, the cooperative is the heartbeat of ambition that formal finance ignores.”

Why Cooperatives Still Matter

Despite recurring failures, cooperatives endure. They are not relics; they are survival tools. In many villages and towns, they remain the only reliable channel for loans, savings, and financial participation. Banks may demand impeccable credit histories, collateral, or digital footprints, but communities demand understanding, empathy, and trust. Cooperatives bridge this gap.

For teachers, civil servants, small-scale farmers, and tourism-adjacent workers, these institutions are more than just financial mechanisms,they are lifelines. They represent the hope that collective effort, guided by shared values, can create opportunities otherwise inaccessible in Botswana’s formal economy.

“When structures are weak, even the noblest intentions crumble.”

The Uncomfortable Truth: Failures Are Structural

Cooperatives fail not because of bad luck, nor solely because of poor leadership. They fail because systems are weak. Across districts and sectors, patterns repeat: boards without financial literacy, AGMs that are attended in formality but not in function, loan policies written on the back of envelopes. Even when funding flows, it often strengthens the fragile structures instead of fixing them.

In short, money alone cannot save what is inherently unstable. The failures are systemic, embedded in governance, culture, and capacity. Understanding this is uncomfortable, but it is necessary. Without confronting these truths, we risk repeating the same mistakes, cycle after cycle.

“Good intentions cannot replace clear rules, and social ties cannot substitute accountability.”

Governance: The Quiet Killer

The most persistent flaw is governance. Social connections often outweigh fiduciary duty. Decisions are guided by relationships, not rules. Boards are populated with well-meaning individuals who lack training in risk management, financial reporting, or accountability. Member oversight exists in theory, not in practice.

Annual general meetings become ritual rather than recourse. Members vote, leaders are elected, and yet the books remain opaque. This is not negligence, it is the natural outcome of underdeveloped systems meeting real human ambition.

“Growth without discipline is fragility in disguise; the bigger they get, the easier they break.”

When Cooperatives Outgrow Their Discipline

The irony is that growth, which should signal strength, often magnifies weakness. Loan books expand without credit risk frameworks. Savings accumulate without proper cash planning. Systems designed for a small group buckle under the weight of success. In these moments, a cooperative is no longer a simple community tool; it becomes a mini-bank, exposed and vulnerable, without the safeguards that banks employ by default.

The lesson is clear: without discipline, expansion becomes fragility. And in Botswana, this lesson is repeated far too often.

“The true strength of a cooperative lies not in its capital, but in the wisdom of its people and the structure that guides them.”

A Pause Before Solutions

Part I ends not with answers, but with observation. The challenge of Botswana’s cooperatives is not that they lack money, ambition, or good intentions. It is that they lack the financial maturity, governance structures, and disciplined culture necessary to protect the resources they already have.

In Part II, we will explore what can be done, how cooperatives can evolve from fragile hope into resilient institutions, and how members, boards, and finance professionals can each play their part in transforming promise into reality.

“When the foundation cracks, you don’t abandon the house, you rebuild it, stronger, wiser, and this time, with everyone holding a brick.”

The question is no longer, “What went wrong?” We’ve heard the answers whispered in villages, mumbled in boardrooms, and echoed through stalled projects. Now, we ask something harder: “What must we do to fix it?“

This piece is not about pointing fingers, that part has been made clear enough on who the guilty parties are. It’s about extending hands, toward community leaders, trust boards, youth, partners, and policymakers who still believe in the idea that development can be dignified, inclusive, and lasting.

Community trusts in Botswana still hold potential, not just as financial entities, but as vessels for transformation. But to unlock that potential, we must be willing to reimagine how they function, who they serve, and how success is measured. This is a call to courage, not criticism. And courage begins with clarity.

We have discussed in detail on what is wrong in part 1. If you’re ready, let’s rebuild. But how do we do that ? This is the focus of our follow up article

“A community cannot own what it does not understand.”

1. Demystify the Trust: Make It Understandable to the People

Too many of our people sit through AGMs like shadows in the back of a hall, present, but excluded. The trust speaks in a language they did not choose. The reports are printed in English. The minutes are buried in filing cabinets. The power, locked behind unfamiliar terms. This is no accident. It is a strategy of control masquerading as procedure.

What must change?

• Translate all trust documents into Setswana and local dialects.

• Host regular “kgotla-style” forums to explain finances in plain terms.

• Replace exclusionary AGMs with public dialogues, where the board must listen.

When people understand what belongs to them, they stop asking for permission. They begin to demand accountability.

“Without truth in the books, there can be no trust in the boardroom.”

2. Audit, Then Clean House

The failure is rarely loud. It’s not some smoking gun. It’s a water tank that never arrives. A classroom project that never finishes. A payment to a cousin’s business. A board member who says, “It was approved,” but never explains by whom.

This is the rot, not dramatic theft, but a slow hemorrhaging of integrity.

Again we ask, what must change?

• Make independent audits mandatory, readable, and publicly posted.

• Set term limits, no more permanent chairs, no sacred cows.

• Introduce citizen-led evaluation panels to track performance.

No one should lead the poor without the burden of proof.

“You cannot run the future with the same minds that buried the past.”

3. Bring Youth and Skills into the Boardroom

Our villages are overflowing with graduates, dreamers, thinkers, and problem solvers. But they are rarely called. Instead, we rotate the same names through committees like furniture, aging, creaking, and immovable.

Wisdom must lead. But not alone. Not forever.

What must change?

•Legally reserve board seats for youth and women.

•Offer mandatory training in financial governance and development strategy.

•Partner with universities to create a pipeline of capable community leaders.

Leadership must not be inheritance. It must be earned, sharpened, and accountable.

“A trust should not just receive, its mission is to multiply.”

4. Turn Trusts into Development Engines, Not Just Revenue Collectors

We have watched trusts survive off concession fees and leases, while schools nearby crumble. We have seen safari companies flourish while villagers wait for tenders that never come. This is not misfortune. It is misdesign.

What must change?

• Launch trust-owned social enterprises, campsites, beekeeping, craft centers.

• Allocate at least 60% of funds to visible, essential development.

• Require each trust to draft, and publicly commit to, a 5-year development roadmap.

A trust with no visible impact is not asleep. It is complicit.

“Power must return to the people who gave it, or it becomes a throne of lies.”

5. Hold Public Leadership Accountable, Ritually

In most of these villages, trust board members are spoken of like ministers. Untouchable. Unquestionable. That is not leadership. That is monarchy. True leadership begins and ends with the people.

What must change?

• Hold quarterly public reviews of trust performance.

• Establish a “Community Recall Clause” to remove inactive or unethical board members.

• Replace secretive procurement with publicly vetted tenders.

If the people cannot correct the course, then they never had the wheel.

“Collaboration should build, not replace.”

6. Strengthen Partnerships Without Losing Ownership

Too often, the biggest buildings in trust land are owned by outsiders. The best jobs go to strangers. The real decisions are made in boardrooms far away. And when the community dares to ask, they’re told: “You signed the agreement.”

But consent without knowledge is not consent. It’s exploitation in formal wear.

What must change?

• Insist on majority community control in all partnerships.

• Have all contracts reviewed by independent legal professionals.

• Track and publish benefit-sharing outcomes from every major deal.

Do not clap for a partnership that leaves your children behind.

“Change must not be promised. It must be proven.”

7. Make Development Visible, Consistently

Trust is not built in announcements. It is built in the muddy foundations of a new borehole. The roof fixed at the school. The medicine delivered to a clinic. These are the signs of integrity. And if they are not seen, they are not real.

What must change?

• Publish annual impact reviews with names, places, faces.

• Host village celebrations for completed projects, big or small.

• Use community radio and art to showcase development.

If your people cannot name what the trust has built, then you have not built anything at all.

“A broken system can either be buried or rebuilt. The difference is whether we still believe we deserve better.”

Reclaiming What Was Meant for Us

Let us say it plainly: community trusts are not dead. They have simply been starved, of clarity, of leadership, of love. But anything starved can be fed. Anything lost can be remembered.

This is not about blame. It is about legacy. Because our children will inherit what we tolerate. And if we want to pass on pride instead of poverty, then we must act, not with slogans, but with structure.

We rebuild by being honest. We rebuild by making space. We rebuild by refusing to clap for mediocrity when justice is possible.

This is the work. This is the moment. And history will ask what we did when we knew.

Authors Note

Why This Matters So Much to Me

“I was raised in a Botswana where stories of land and heritage shaped our mornings, and where the word “community” meant something sacred. Later, I found myself working inside an industry built on that same land, one that trades in the wonder of our wilderness, but often forgets the people who breathe life into it.

This matters to me because I’ve seen both sides. I’ve worn the suit, attended the meetings, reviewed the budgets. But I’ve also stood in villages where promises echo louder than progress. Where the trust meant to be a lifeline has become a locked box, and no one knows who holds the key.

I don’t write this as an outsider. I write this as someone still in it, someone who believes that we can serve both conservation and community, but only if we are brave enough to stop pretending everything is fine.

I write this because I owe it to the child I was, the professional I’ve become, and the country I love.“

Kesaobaka Pelokgale

Call to Action If you are a board member, step up. If you are a villager, speak up. If you are a policymaker, show up.

Because this was never a favour. It was always ours. And it’s time we reclaimed it.

“Promises made in the shadows of luxury tents echo like ghosts in the villages left behind, and where hope was meant to grow, silence took root instead.”

In the belly of Botswana’s tourism economy, where luxury tents rise higher than classrooms and safari trucks pass more frequently than ambulances, lies a truth too many pretend not to see. Behind the roaring lions, the champagne sunsets, and the billion-pula industry, there exists a promise made to our people. A promise carried by names like Sankuyo, Khwai, Mababe, Okavango, and Chobe Enclave, community trusts born from a vision: “to ensure that the land, the animals, and the revenue they produce would finally feed more than just the tourism elite.”

These trusts were meant to be the bridge between rural life and national prosperity. The idea was beautiful, empower the very communities coexisting with wildlife, make them custodians of both ecology and economy, and let tourism fund development where government budgets rarely reach. A moral economy, rooted in justice, stewardship, and equity.

And yet, today, most Batswana cannot tell you what a community trust does. Many living within these communities have never seen a balance sheet, never attended an AGM, and never questioned why their children’s school still has pit latrines while tourists pay thousands of U.S dollars per night next door. That silence is not by accident. It is by design.

“To give a man ownership but deny him control is to chain his spirit behind a golden cage.”

The Illusion of Empowerment

On paper, community trusts are among the most radical tools of empowerment ever imagined on African soil. They were designed to shift the power dynamic, to give the community not just a seat at the table, but the right to own the table itself. But somewhere between legislation and implementation, empowerment became ceremonial.

The language of “community ownership” is everywhere, in reports, in contracts, in speeches. But ownership, in practice, requires control. And most communities have little or no control over how their trust is run, how funds are spent, or who represents them. Leadership selection processes are often opaque. Voting is limited to a select few. Financial reports, if they exist at all, are unreadable to the average person or never shared. The result? A trust structure that promises empowerment but delivers dependency. A system where the community claps on cue, but never gets to speak.

There is something especially cruel about being told you own something you can’t touch.

“When trust is broken piece by piece, the cracks become the graveyards of dreams.”

The Collapse of Trust (Literally and Figuratively)

The word trust is sacred. It implies belief, reliability, a contract of honor between parties. But in many cases, community trusts have collapsed that belief. Not through one dramatic theft, but through a thousand small fractures, delayed reports, missing funds, unfulfilled projects, years of “planning” that never materialize into development.

Financial mismanagement isn’t always dramatic. Often, it’s subtle: vehicles bought for “operations” but used for personal errands. Travel allowances that exceed the value of the projects being reviewed. Contractors paid for work no one checks. Board members who travel to tourism expos in foreign countries while villagers wait for basic infrastructure. These practices bleed the trust dry while giving the illusion of activity.

Over time, even well-meaning leaders become defensive, gatekeeping knowledge instead of sharing it. Transparency becomes a threat. Accountability, an inconvenience. And the trust, the thing meant to uplift, becomes just another institution the community no longer believes in.

“Ignorance is the quietest weapon—used not to protect, but to imprison.”

The Weaponization of Ignorance

Perhaps the most sinister failure is not financial, but educational. The fact that most Batswana, across rural and urban divides, have no idea what a community trust is, how it operates, or what rights they have within it, is not a coincidence. It’s strategy.

By keeping financial reports complicated, governance structures vague, and meetings exclusive, communities are locked out of the very systems created for them. And when people are uninformed, they are easier to appease. A gift here. A promise there. An announcement that a “feasibility study” is underway. Hope is dangled just long enough to prevent outrage, and ignorance becomes the currency that sustains a broken structure.

The tragedy here is that our people are not incapable. They are just uninformed, deliberately so. In a country as educated and resource-rich as Botswana, that’s an indictment of the system, not the people.

“Silence in the face of injustice is the loudest betrayal of all.”

When Accountability Becomes Taboo

The power of accountability is that it asks questions no one wants to answer. And in many communities, to ask those questions is to be labeled a troublemaker. You will be told you are dividing the community. That you are envious. That you are working with outsiders to destroy something sacred.

So, people stop asking. They stop attending meetings. They stop reading the notices. They grow disillusioned. And the silence is interpreted as approval.

But let’s be clear: silence is not consent. It is exhaustion. It is the heavy sigh of a people who have been promised too many times, and seen too little. When leaders no longer fear the people’s questions, they forget who they serve.

“True power is returned not when you take back control, but when you give it back with open hands.”

Reclaiming the Promise

Community trusts can still work. They are not inherently flawed. In fact, when run with integrity, they remain one of the most promising models of grassroots economic development anywhere in Africa.

But to reclaim that promise, we must first confront the truth. These trusts are not failing because of a lack of resources. They are failing because of a lack of will, a lack of integrity, and a lack of accountability.

We need independent audits that are accessible to the community. We need AGMs where real questions are asked and answered. We need youth involved, not just as observers, but as participants with voting rights and leadership potential. We need to de-politicize trust boards and replace tokenism with training.

And perhaps most of all, we need to return to the very reason these trusts were formed: to serve the people. Not the board. Not the consultants. Not the safari operators. The people.

“If we cannot trust the trust meant to build us, then all that remains is the rubble of broken promises.”

A community trust is more than an institution. It is a covenant, a sacred agreement between the people, the land, and their future.

If that covenant is broken, we are not just losing money. We are losing hope. We are raising generations who see tourism not as opportunity but as exploitation. Who believe that development is something that happens elsewhere. Who are taught, by silence and inaction, that nothing ever really changes.

But that does not have to be our legacy. We can still rewrite this story. We can still demand better. Not by asking politely, but by insisting, relentlessly, that trust must be earned, and if broken, rebuilt.

Because if a trust cannot be trusted, then what are we even building?

“Somewhere between the mission and the meetings, the people were forgotten.”

Author’s Note “I’ve worked in the safari industry. I still do. I’ve seen the beauty it brings and the billions it moves. But I’ve also seen what doesn’t get talked about, the broken boreholes, the empty promises, the leaders who forget why they were chosen. This isn’t an outsider’s rant. It’s an insider’s reckoning. I write this not out of anger, but out of duty. Because I know what this industry could be if it truly served the people who live with the land, not just those who profit from it.'”

Build no thrones for the untested, let the fire kiss their bones, let the climb tear their pride. Only then will the crown fit.

We have become a society afraid to question, afraid because of “Cancel culture“, understand that I am a firm believer in equality, but woke culture should not distort the meaning of true progress. I grew up watching my mother, move through life like a force of nature, unyielding, resolute, and proud. She didn’t get where she is because someone handed her a seat at the table or because of hollow policies. No, her triumphs are carved from years of struggle, sweat, and sacrifice. I remember her late nights,alone, bent over worn papers, the faint glow of those weird lights she bought from China Shops, the only witness to her battle. She wasn’t a token. She wasn’t a checkbox. She was a warrior who earned every inch of her ground. Her story is no different from those of many other champion women.

This is what true empowerment looks like.

And yet today, I ask myself, and I ask you, are we diluting this legacy? Are we replacing struggle with entitlement? Are we telling our daughters that success is a right to be given instead of a mountain to be climbed?

Do we raise them to expect a path smoothed by quotas and policies? Because, as a father, this unsettles me deeply. Is that the world I want for my daughter? One where victories come easy, and character takes a back seat?

Character is not built in comfort. It is forged in fire,in the heat of obstacles, the smoke of sacrifice, and the scars earned from pushing past failure.

There is a danger in comfort. It lulls ambition to sleep. When equality becomes a box to tick, when inclusion is reduced to a quota, we teach a dangerous lie: that effort is optional, that merit is negotiable.

We risk creating not empowered women, but complacency disguised as progress.

This is not progress!!

Real empowerment is raw and relentless. It respects the journey as much as the destination. It refuses shortcuts and empty gestures.

My mother’s story, and the stories of countless women like her, remind us that strength is not given; it is earned.

We must resist the temptation to force equality into neat boxes. Equality is not a product to be packaged and delivered; it is a living, breathing challenge. It unsettles the comfortable. It demands our best selves. It asks us to grow.

The risk of forcing equality is that we turn a noble goal into a hollow ritual. We breed resentment in those who feel unearned privilege and mediocrity in those denied the crucible of challenge.

We lose sight of the very essence of empowerment: the triumph of character.

At the heart of this struggle lies a simple truth: character is the only true currency. It cannot be granted, borrowed, or bought. It is earned through the hard work of standing tall when the world pushes you down. It is shaped by the choices we make in the face of adversity.

So I ask you,if true equality demands discomfort, if it asks us to reject the easy path, are we prepared to pay that price? Are we willing to teach our daughters that empowerment is not a gift, but a responsibility? That strength is not handed down, but wrestled from life’s challenges?

Because anything less than this is a betrayal. A betrayal of those who fought before us, and a disservice to those who will come after.

And where does this leave our sons?

Do we raise them to feel entitled to privilege? To be exempt from struggle? Or do we challenge them to be better men,not through inherited power or blind entitlement, but through integrity, discipline, and humility?

True equality demands that our sons and daughters alike learn the value of effort. That they understand the dignity in hard work and the grace in perseverance.

Raising sons who are comfortable with discomfort,who know that real strength is gentleness forged in discipline,is just as vital as empowering daughters.

Because a society that demands easy victories from one gender and relentless struggle from another is no society at all. It is fractured.

If we are to move forward, we must reject easy narratives and empty tokens. We must teach our sons and daughters alike that empowerment is hard. That equality is messy. That the prize is never given,it is earned, over and over again.

This is not a rejection of progress, but a call for honesty.

A call to stop confusing equality with entitlement.

A call to reclaim the soul of empowerment,grounded in merit, struggle, and character.

So, I challenge you,whether you are a parent, a leader, or a thinker,to stop seeking comfort in easy answers. Ask yourself: Are we building strength, or are we breeding complacency?

Are we raising a generation that will stand tall because they earned their place? Or one that will stumble because they expected it handed to them?

Because in the end, equality is not a destination. It is a fire.

And every day, it demands to be stoked,not with comfort, but with courage.

If you take nothing else from this, take this:

Character is not a gift. It is earned. The only true equality is the equality of effort.

“Public funds are not numbers on a spreadsheet, they are the lifeblood of our nation’s hope. Every misused thebe is a stolen dream.”

As someone who has walked the corridors of finance in both the public and private sectors, I write this not only with a sense of professional responsibility but with a heart heavy with concern for our country’s future. The misallocation and misuse of public funds is not just a line item in an audit report, it is a betrayal of trust, a delay in progress, and a disservice to every hardworking Motswana who dreams of a better tomorrow. This piece is not politically motivated and definitely not meant to speak against the previous or current regime. It is directed to the individual citizen and the civil servants who are the harbingers of this uncertain fate, regardless of political affiliation.

What we can no longer ignore is that we cannot afford to treat public funds as anything less than sacred. Every single thebe that enters government coffers represents potential, potential to build, to heal, to educate, and to empower. When that money is mishandled, wasted, or stolen, it is not the government that suffers,it is the people. It is us. This article focuses on how to combat against the gross misuse of public funds and the future that awaits us if we do not stand firm in our resolve.

“Integrity isn’t built on promises, but on systems that make wrong-doing difficult and honesty second nature.”

Build Systems That Hold People Accountable

Effective public financial management starts with accountability. Accountability is not just about punishing wrongdoing, it’s about creating systems that make wrong-doing difficult in the first place. Too often, we rely on manual processes, outdated controls, and informal oversight mechanisms that create gaps wide enough for corruption and mismanagement to thrive.

Segregation of Duties: We need clearly defined roles and responsibilities so that no one person has complete control over any financial transaction. If one person can initiate, approve, and disburse funds, the system is inherently flawed. Dividing these roles reduces the opportunity for abuse.

Independent and Frequent Audits: Internal and external audits should not be rare events or tick-box exercises. They should be frequent, thorough, and independent of influence. Risk-based auditing, targeting areas most vulnerable to misuse, must become standard practice.

Lifestyle Audits: We must normalize lifestyle audits for public officials. If a person’s standard of living significantly exceeds their known income, it should raise a flag. These audits serve as a deterrent and promote a culture of honesty in public service. Building these systems isn’t about suspicion, it’s about responsibility. We owe it to our people to safeguard their resources with the same rigor we would protect our own households.

“In a digital age, ignorance is no longer an excuse and opacity no longer a shield. Let transparency be coded into every transaction.”

Let Technology Be Our Watchdog

We are living in an era where technology can be our greatest ally in the fight for financial integrity. Unfortunately, many of our systems are still trapped in analog processes and paper trails that are easy to manipulate and difficult to trace.

E-Procurement Platforms: Digital procurement platforms automate bidding, evaluation, and payment processes, reducing the room for under-the-table deals. These systems log every step, making it easier to audit and verify the process.

Blockchain Technology: Blockchain offers transparent, tamper-proof financial records. With this, every transaction is logged in a way that cannot be edited or hidden. It creates a permanent record that anyone can verify.

AI and Data Analytics: Advanced analytics and machine learning can flag suspicious transactions in real time. These technologies help identify patterns and anomalies that a human might overlook, making fraud detection faster and more accurate. Implementing these tools is not about replacing people, it’s about empowering them to do their jobs better, and more ethically.

“Justice is not real until it is felt by all, especially when it is inconvenient. No badge, no title, no seat should stand above accountability.”

Enforce the Law, Without Fear or Favor

Misusing public funds is theft. Let’s call it what it is. And like any theft, it should carry consequences. But enforcement only works when it is impartial, consistent, and unrelenting.

Whistleblower Protection: We must create a safe environment for individuals to report financial misconduct. Whistleblowers should be praised for their courage, not punished for their honesty.

Tough Penalties: When people misuse public funds, there must be meaningful consequences, fines, dismissal, criminal charges. Justice must be visible and firm to serve as a deterrent.

Independent Oversight Bodies: Institutions like anti-corruption units such as the DCEC, audit offices, and ombudsmen must operate free from political interference. Their independence is key to ensuring that investigations and enforcement are not compromised.

If we want to instill trust in the system, we must show that no one is above the law. Not politicians. Not CEOs. Not civil servants.

“True democracy isn’t just about casting votes, it’s about knowing where every thebe of your tax goes and having the voice to question it.”

Put Power in the People’s Hands

Citizens should not be passive observers of how their taxes are spent. When the public is engaged in budgeting and monitoring, it not only increases transparency but also improves the effectiveness of public spending.

Participatory Budgeting: Citizens should be involved in setting priorities, especially at the local level. When people decide where money goes, it’s far more likely to be spent wisely.

Community Monitoring: Civil society organizations and watchdog groups must be supported in monitoring government projects. Whether it’s a school being built or a road being tarred, someone from the community should be able to verify that the work is being done and the money is being used properly.

Public Financial Transparency: Budgets, procurement data, and spending reports should be accessible to all. Open data portals allow citizens, journalists, and researchers to track and analyze public spending. Engaged citizens are the best defense against corruption. When people are informed and involved, the space for misuse shrinks dramatically.

“A nation can survive flawed policy, but never normalized dishonesty. Culture eats compliance for breakfast, let’s nourish the right one.”

Culture and Competence Matter

Even the best systems can fail if the people operating them lack integrity or competence. That’s why ethics and training are just as important as policies and procedures.

Training Public Servants: Continuous education on finance laws, procurement regulations, and ethical conduct should be mandatory. Many errors are not malicious, they stem from ignorance. Training solves that.

Enforcing a Code of Conduct: A clear, enforced code of ethics sets expectations for behavior. Violations should carry consequences, not just in law, but in professional reputation.

Leading by Example: Ethical leadership at the top inspires accountability at every level. Leaders must not only talk the talk but walk the walk.

A culture of integrity is built from the inside out. It starts with values, and values must be lived.

“We may not control how history remembers us, but we do control what we stand for. Let ours be the generation that chose courage over silence.”

This is not just a professional plea, it’s a personal one. I love this country. I love its people. I believe in our potential. But we cannot reach it if we continue to allow our resources to be drained by greed, negligence, or inefficiency.

Misusing public funds is not a victimless crime. It is a stolen classroom. A delayed hospital. An unfinished road. It is opportunity lost, and dignity denied.

We must act. We must reform. And most importantly, we must care. Because financial integrity is not a technical issue, it is a moral one. And the time to fix it is now. Let us not be remembered as the generation that watched silently while things fell apart. Let us be remembered as the generation that stood up, spoke out, and fixed what was broken.

Our country, our people, and our future deserve nothing less.

“An economy that clings to old ideas risks suffocating the innovations of tomorrow.”

Botswana’s economy has long been celebrated as one of Africa’s great success stories. Fuelled by diamonds and bolstered by prudent fiscal management, our country has enjoyed decades of stability and growth. But beneath this polished exterior lies a growing sense of urgency. Recent economic challenges, high unemployment, inflationary pressures, and slow progress in diversification are exposing the consequences of questionable decisions made in the past.

As we stand at this critical juncture, it’s time to reflect on where we’ve been, acknowledge our missteps, and chart a new course for the future.

“An economy built on one resource is like a house with one pillar—strong until the winds of change blow. Diversification isn’t optional; it’s survival.”

The Legacy of Diamonds: A Double-Edged Sword

Botswana’s diamond wealth has been both a blessing and a curse. While it has built infrastructure, funded education, and provided a buffer against economic shocks, it has also created a dependency that now leaves the economy vulnerable and at risk of fluctuations within the global market. As diamond prices are influenced by international demand, any downturn can trigger significant economic challenges for the nation.

For years, experts have called for diversification to reduce reliance on diamonds, with many highlighting the importance of exploring alternative sources of revenue that can offer more stability. And while some progress has been made in tourism, financial services, and agriculture, these sectors have not grown fast enough to fill the gap left by diamonds. In addition to this slow growth, the challenges that these sectors face, such as infrastructure deficits and limited marketing, pose significant obstacles. The reality is that diversification has often been more of a talking point than a fully realised strategy, leading to concerns about the sustainability of Botswana’s long-term economic outlook.

“Every questionable decision echoes in the lives of those it impacts. Leadership without accountability is a slow erosion of trust.”

Questionable Decisions and Missed Opportunities

Some of the challenges Botswana faces today stem from decisions or, in some cases, indecision on key areas:

1. Infrastructure Development Delays While Botswana has invested heavily in infrastructure, many projects have suffered from delays, cost overruns, or inefficiencies that plague effective execution. Gaps in areas like water security and energy production have constrained economic growth and created unnecessary vulnerabilities, severely impacting industries reliant on reliable supply.

2. Underutilisationof Human Capital Botswana’s youth unemployment rate is one of the highest in the region, hovering around 35%. For a country with a well-educated population, this is a glaring issue that highlights a misalignment between the skills of the labour force and the needs of the job market. Many government programs aimed at addressing unemployment have failed to align with the skills demanded by the private sector, leaving graduates stranded without opportunities and resulting in a brain drain as talented individuals seek roles abroad.

3. Inefficiencies in Government Spending While Botswana’s public debt remains manageable, concerns about the efficiency of government spending are growing as more scrutiny is directed at underperforming sectors. Significant funds are directed toward subsidies and underperforming state-owned enterprises, often with little accountability, causing concern among citizens and stakeholders alike. This drains resources that could be better used to invest in innovation and growth sectors, essential for refreshing the economy.

4. Slow diversification efforts Opportunities in renewable energy, technology, and agribusiness remain underexplored, even though these industries have the potential to drive growth and create jobs in a sustainable manner. The lack of strategic investment in these areas, coupled with bureaucratic red tape and a lack of urgency, has hampered progress in these sectors significantly.

“Botswana’s strength lies not just in its resources, but in its people. When we empower them, we unlock our true wealth.”

The Current Climate: A Snapshot of Challenge

These past decisions are now coming home to roost, as evidenced by several pressing economic issues:

High Unemployment: Botswana’s job market struggles to absorb the growing youth population, creating widespread disillusionment and contributing to social unrest as young people seek opportunities that are out of reach.

Rising Inflation: Dependence on imports, particularly for food and energy, has exposed the country to external price shocks, pushing up the cost of living and creating greater economic disparity.

Limited Economic Resilience: The economy’s vulnerability to global diamond demand underscores the need for stronger, more diversified revenue streams, especially in a time when economic conditions are becoming more volatile and unpredictable.

“The greatest growth often stems from the hardest challenges. Opportunity is born in the fires of adversity.”

A Path Forward: Turning Challenges Into Opportunities

Despite these challenges, Botswana’s potential remains immense. The recent change in government has brought renewed focus on addressing these pressing issues with fresh policies aimed at fostering economic resilience. The new administration has expressed a commitment to diversification strategies, seeking to harness the country’s natural resources and human capital more effectively. The country’s recent adjustment to the Pula exchange rate framework is a positive step, signalling a willingness to adapt and compete in a globalised economy. But more comprehensive measures are needed to truly shift the trajectory of the economy, enabling it to harness fully the capabilities of its citizens and natural resources.

1. Fast-track Diversification Botswana needs bold, decisive action to expand into new industries that are less susceptible to external fluctuations. Renewable energy, for instance, is an area where the country has natural advantages,abundant sunlight and land, offering immense potential for growth. Similarly, investing in technology and innovation could position Botswana as a leader in the digital economy, allowing it to tap into global markets and create sustainable jobs.

2. Invest in People Education and training must be aligned with market demands to equip the youth with relevant skills. Programs that focus on upskilling and entrepreneurship can empower young people to act as catalysts for economic growth. Instead of relying solely on government-led initiatives, fostering partnerships with the private sector will be key to ensuring that practical experiences and mentorship are available to the youth.

3. Streamline Government Spending Efficiency and accountability should be at the core of public spending practices. Resources must be directed toward projects and industries with high growth potential while underperforming initiatives are re-evaluated or phased out for better allocation of national resources. This shift can enhance the public’s trust in government capacity to stimulate economic progress.

4. Leverage global trends Botswana must embrace emerging global trends, such as green technology and AI, to create a competitive advantage. By investing in these areas, the country can attract foreign investment, which in turn can generate jobs in high-growth sectors and foster an economy that thrives in innovation and creativity.

“The future rewards those who dare to look beyond comfort zones and make decisions that ripple through generations.”

A Time for Reflection and Renewal

Botswana has a proud history of economic success, but resting on past laurels is no longer an option. The cracks in our economic foundation are clear, and the decisions we make today will determine whether we emerge stronger or fall further behind the global curve.

This is a moment for bold leadership; a chance to confront uncomfortable truths about our past decisions and commit to a future that is innovative, inclusive, and sustainable. With the fresh perspectives brought in by the new government, Botswana has the resources, the talent, and the resilience to rise to the challenge. What’s needed now is the vision and courage to make it happen, ensuring that all voices are heard in the process of nation-building.

The past has brought us here, but the future is ours to shape. Let’s seize this opportunity to build an economy that reflects the potential of our diverse populace and secures prosperity for generations to come, forging a path that moves beyond dependency, fostering empowerment and self-sufficiency.

“Managing cash flow effectively is the lifeline of any SME. Credit can stabilize your finances, but only if it’s managed with precision.”

Running a small or medium-sized enterprise (SME) is a constant balancing act, where every decision can significantly impact your business’s success and sustainability. As an entrepreneur, you understand the importance of keeping operations smooth and seizing growth opportunities whenever they arise. However, achieving these goals often requires more financial resources than what’s readily available. This is where credit comes into play. Whether you’re considering taking out a loan to expand your business or offering credit terms to your customers to boost sales, operating on credit can be both a powerful tool and a potential pitfall. Understanding the benefits and challenges of utilizing credit is crucial for navigating the complexities of business finance and ensuring your SME thrives in a competitive market.

Benefits of Operating an SME on Credit

“Credit can be the fuel that powers your business’s growth engine. Used wisely, it transforms potential into reality.”

Borrowing from Financial Institutions

1. Improved Cash Flow Management Access to working capital is vital for SMEs. Credit facilities, such as lines of credit and short-term loans, provide the necessary funds to manage daily operations smoothly. This financial cushion helps businesses handle cash flow fluctuations caused by delayed receivables or seasonal variations. Moreover, having credit available offers flexibility, enabling SMEs to cover unexpected expenses or capitalize on sudden opportunities without disrupting their operations.

2. Facilitating Growth and Expansion Credit plays a significant role in funding expansion projects. Whether it’s opening new locations, purchasing advanced equipment, or increasing inventory, borrowed funds can propel growth. Additionally, credit allows SMEs to invest in research and development, adopt new technologies, and innovate, which are crucial for staying competitive in the market.

3. Building Creditworthiness Regular and responsible borrowing helps SMEs establish a solid credit history. This can lead to better credit terms and increased borrowing capacity in the future. Good creditworthiness can also enhance supplier relationships, leading to more favorable terms such as extended payment periods or bulk purchase discounts.

4. Financial Leverage Using debt financing allows SMEs to leverage their equity capital, potentially increasing returns on equity. If the returns generated by the investment exceed the cost of debt, this financial leverage can significantly boost profitability.

“Extending credit to customers is an investment in loyalty and sales growth. However, clear policies and diligent management are essential.”

Extending Credit to Customers

1. Boosting Sales and Customer Loyalty Offering credit to customers can lead to increased sales by making purchases more accessible. Customers are more likely to buy when they can pay later. Providing trade credit can also enhance customer loyalty and foster long-term relationships, as customers appreciate the flexibility.

2. Competitive Advantage SMEs that offer favorable credit terms can differentiate themselves from competitors. This competitive edge can attract more customers and provide leverage in negotiations, allowing for better terms or higher prices.

Challenges of Operating an SME on Credit

Borrowing from Financial Institutions

1. Risk of Over-Indebtedness: Relying too heavily on credit can lead to excessive debt accumulation, making it challenging to meet financial obligations. High interest rates and fees associated with borrowing can erode profit margins and strain finances.

2. Cash Flow Impact: Regular debt repayments can put a strain on cash flow, particularly during downturns or when unexpected expenses arise. High debt servicing costs can reduce the amount of available cash for other essential business activities, such as marketing, hiring, or product development.

Access to Credit: SMEs may face difficulties accessing credit if they lack a strong credit history or sufficient collateral. This can limit their ability to finance growth or manage cash flow effectively. Lenders may also impose stringent terms, such as high collateral requirements or personal guarantees, which can limit operational flexibility.

Economic and Market Risks: Changes in interest rates can affect borrowing costs, with rising rates increasing debt servicing costs. Additionally, economic downturns or market volatility can impact an SME’s ability to generate revenue and meet debt obligations. In challenging economic conditions, access to credit may become more restrictive, exacerbating financial difficulties.

Extending Credit to Customers

1. Risk of Non-Payment Extending credit to customers increases the risk of non-payment, leading to bad debt and financial losses. Effective credit management practices are required to mitigate this risk, adding to operational complexity.

2. Cash Flow Constraints Offering credit to customers can delay cash inflows, potentially leading to cash flow constraints. This can tie up working capital, reducing liquidity for other business needs.

3. administrative Burden Managing customer credit accounts requires ongoing monitoring and administrative effort, which can be resource-intensive. SMEs may need to invest in resources and processes to follow up on overdue accounts and collect payments.

Tackling the Challenges

Successfully navigating the challenges of operating on credit requires strategic planning and disciplined financial management. Here are some key strategies:

1. Prudent Borrowing Practices Assess Your Needs: Only borrow what you need and can afford to repay. Carefully evaluate how the borrowed funds will be used and the expected return on investment. Shop Around: Compare different lenders and their terms. Look for the best interest rates and repayment terms that align with your business needs. Maintain a Healthy Balance: Avoid over-reliance on debt. Strive for a balanced mix of debt and equity financing to mitigate the risk of over-indebtedness.

2. Effective Cash Flow Management Monitor Cash Flow: Regularly track your cash flow to ensure you have sufficient liquidity to meet your obligations. Use cash flow forecasts to anticipate and prepare for potential shortfalls. Optimize Payment Terms: Negotiate favorable payment terms with both lenders and suppliers. Aim to extend payment terms with suppliers while reducing credit terms for your customers to improve cash flow.

3. Robust Credit Management Conduct Credit Checks: Before extending credit to customers, perform thorough credit checks to assess their creditworthiness. This can help reduce the risk of non-payment. Set Clear Credit Policies: Establish and enforce clear credit policies, including payment terms, credit limits, and collection procedures. Ensure your customers are aware of these policies. Automate Invoicing and Collections: Use accounting software to automate invoicing and follow-up reminders. This can help streamline the credit management process and reduce the administrative burden.

4. Build Strong Relationships with Lenders Communicate Regularly: Maintain open lines of communication with your lenders. Keep them informed about your business’s financial health and any significant changes. Demonstrate Creditworthiness: Consistently meet your repayment obligations to build a strong credit history. This can lead to better borrowing terms and increased access to credit in the future.

5. Mitigate Economic and Market Risks Diversify Revenue Streams: Diversify your customer base and revenue streams to reduce dependency on any single source of income. This can help cushion the impact of economic downturns. Monitor Economic Indicators: Stay informed about economic trends and market conditions that could affect your business. Be proactive in adjusting your strategies to mitigate potential risks.

“Effective credit management requires dedication and the right tools. Streamlining processes can turn a potential burden into a strategic advantage.”

Operating an SME on credit, whether through borrowing from financial institutions or extending credit to customers, offers significant benefits such as improved cash flow management, facilitated growth, and enhanced customer relationships. However, these advantages come with challenges, including the risk of over-indebtedness, cash flow constraints, and the administrative burden of credit management.

By adopting sound financial management practices, such as prudent borrowing, effective cash flow management, robust credit policies, and maintaining strong lender relationships, SMEs can leverage the power of credit to drive growth and sustain long-term success. Understanding and addressing the challenges associated with credit will enable entrepreneurs to navigate the complexities of business finance confidently and ensure their enterprises thrive in a competitive market.

“Good governance is the single most important factor in eradicating poverty and promoting development.” — Kofi Annan, former Secretary-General of the United Nations

In recent years, corporate governance and ethics have become increasingly important in Sub-Saharan Africa as the region continues to experience significant economic growth and development. Ensuring that businesses operate with high standards of governance and ethical behavior is critical to sustaining this progress, attracting investment, and fostering inclusive development.

As Sub-Saharan Africa emerges as a hub of economic activity, the spotlight on corporate governance and ethics intensifies. This article delves into the crucial role these principles play in shaping the business landscape of the region and why their adherence is paramount for its continued advancement.

Let’s explore how the integration of robust corporate governance practices and ethical behavior not only bolsters the credibility of businesses but also underpins sustainable growth and fosters a culture of accountability and transparency.

“The effectiveness of the board is critical to the health and performance of the company. A well-composed, independent board can provide the necessary checks and balances.”

What is Corporate Governance?

Corporate governance refers to the system by which companies are directed and controlled. It encompasses the mechanisms, processes, and relations used by various parties to control and to operate corporations. These include the distribution of rights and responsibilities among different participants in the corporation (such as the board of directors, managers, shareholders, creditors, auditors, regulators, and other stakeholders) and the rules and procedures for making decisions in corporate affairs. Corporate governance provides the structure through which company objectives are set, and the means of attaining those objectives and monitoring performance.

The Importance of Corporate Governance and Ethics

Economic Growth and Investment

Good corporate governance and ethical practices enhance the credibility and reputation of businesses, making them more attractive to investors. Transparency, accountability, and effective risk management practices reassure both local and international investors about the stability and sustainability of businesses in the region.

Sustainability and Development

Strong governance frameworks and ethical conduct contribute to sustainable development by promoting responsible business practices. This includes respecting environmental standards, upholding human rights, and engaging with local communities. In Sub-Saharan Africa, where many countries are rich in natural resources, sustainable and ethical exploitation of these resources is crucial for long-term prosperity.

“We do not only inherit the earth from our ancestors, we borrow it from our children.” — Native American Proverb

Key Elements of Corporate Governance in Sub-Saharan Africa

Board Composition and Independence

A balanced and independent board of directors is essential for effective governance. There is a growing recognition of the need for boards to include independent directors who can provide objective oversight and mitigate conflicts of interest. However, finding qualified and independent directors can be challenging in some countries due to limited pools of experienced professionals.

Stakeholder Engagement

Engaging with a broad range of stakeholders, including employees, customers, suppliers, and local communities, is critical. Businesses in the region are increasingly adopting inclusive approaches to stakeholder engagement, recognizing that addressing the concerns and expectations of diverse groups can enhance their social license to operate and support long-term success.

Transparency and Disclosure

Transparency in financial and non-financial reporting builds trust with stakeholders. In Sub-Saharan Africa, efforts are being made to improve transparency and disclosure practices. This includes adherence to international financial reporting standards and increased emphasis on disclosing environmental, social, and governance (ESG) metrics.

Risk Management

Effective risk management is vital in a region where businesses often face unique challenges, such as political instability, economic volatility, and infrastructure deficits. Companies are focusing on identifying and mitigating risks through comprehensive risk management frameworks, which help ensure resilience and continuity.

“Fighting corruption is not just good governance. It’s self-defense. It’s patriotism.”

Ethical Challenges and Opportunities

Corruption!!

Corruption remains a significant challenge in Sub-Saharan Africa, undermining governance and ethical standards. Businesses must navigate complex environments where corrupt practices can be pervasive. Combating corruption requires a firm commitment to ethical behavior, supported by robust anti-corruption policies and practices.

Corporate Social Responsibility (CSR)

Corporate social responsibility is gaining traction in the region. Companies are increasingly recognizing their role in contributing to social and economic development. Effective CSR initiatives can enhance a company’s reputation, build stronger community relationships, and create a more favorable operating environment.

Regulatory Environment

The regulatory landscape in Sub-Saharan Africa is evolving, with many countries strengthening their corporate governance and ethical frameworks. Governments and regulatory bodies are introducing new laws and regulations aimed at improving business practices, protecting investors, and promoting transparency. However, enforcement remains inconsistent, and businesses must navigate varying regulatory requirements across the region.

Technological Advancements

The rapid adoption of technology presents both opportunities and challenges for governance and ethics. On one hand, technology can enhance transparency, improve stakeholder engagement, and streamline compliance processes. On the other hand, it introduces new ethical dilemmas, such as data privacy concerns and the need for robust cybersecurity measures.

“Effective regulation ensures that the rules are fair and protect all stakeholders, fostering a healthy business environment.”

Corporate governance and ethics are critical to the continued growth and development of businesses in Sub-Saharan Africa. As the region integrates more deeply into the global economy, adopting and upholding high standards of governance and ethical behavior will be essential for attracting investment, fostering sustainable development, and ensuring long-term success. Companies must remain vigilant and proactive, continuously adapting to emerging challenges and opportunities to build trust and create value for all stakeholders.

By prioritizing these principles, Sub-Saharan Africa can not only enhances its economic landscape but also set a global example for responsible and sustainable business practices.

“Botswana’s quest for economic liberation begins with dismantling the barriers of oligopoly, paving the way for a landscape where competition thrives, innovation flourishes, and opportunity knows no bounds.”

In the intricate tapestry of Botswana’s economic landscape, a select few wield significant influence, steering the course of entire industries. These entities, akin to modern-day economic titans, operate within the realm of oligopolies, where power is concentrated in the hands of a privileged few. Much like the ubiquitous board game Monopoly, where players vie for control over properties and resources, oligopolies dictate the flow of commerce and shape the livelihoods of millions.

But beyond the confines of a game board lies a reality where the stakes are real, and the consequences profound. In Botswana, oligopolistic forces exert their dominance across various sectors, from banking and retail to telecommunications and energy. Yet, beneath the surface lies a dichotomy of opportunity and peril, where the promise of prosperity is tempered by the perils of market manipulation and consumer exploitation.

As we embark on this journey of exploration, we invite you to peer behind the curtain and unravel the mysteries of oligopolies in Botswana. Through insightful analysis and actionable insights, we aim to demystify these economic behemoths and chart a course towards a more equitable and vibrant economy. Join us as we delve into the intricacies of oligopolistic power dynamics, and discover the transformative potential of fostering competition and consumer empowerment in Botswana’s economic landscape.

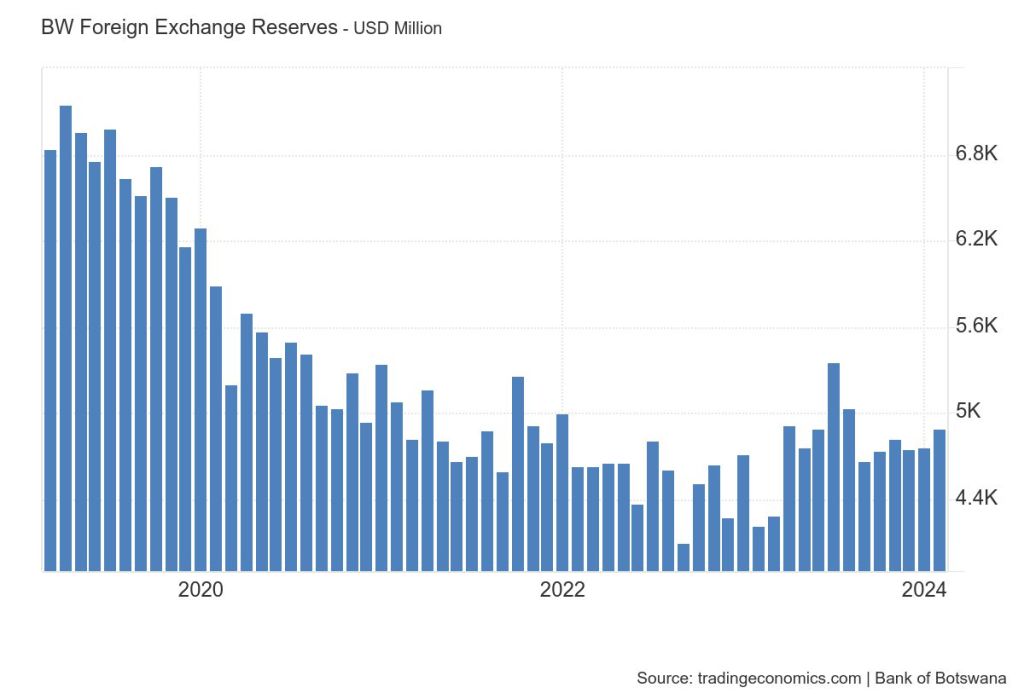

“Foreign reserves are not just numbers; they are the lifeline of a nation’s economic sovereignty.”

As citizens of Botswana, we have always been proud of our country’s stable government and thriving economy. Central to its economic resilience is the prudent management of foreign reserves, which plays a pivotal role in safeguarding the country’s financial stability and supporting its economic growth trajectory.. In this short read, we explore why these reserves are so vital for the country’s prosperity.

The Story Behind Botswana’s Foreign Reserves

“The strength of a nation’s foreign reserves reflects the strength of its economy.”

Since gaining independence in 1966, Botswana has strategically leveraged its abundant diamond resources to build robust foreign reserves. It is important to note that the foreign reserves are not solely dependent on diamonds. While diamonds and other minerals have historically been a major contributor, revenue from other sectors tourism, agriculture, and services also plays a significant role. Therefore, Botswana’s foreign reserves are the result of a diverse range of economic activities and sources of income. The government, through the Bank of Botswana, has implemented sound policies to manage these reserves effectively, ensuring their availability to weather economic uncertainties and capitalize on growth opportunities.

Why Foreign Reserves Matter

“Foreign reserves serve as a shield, protecting the economy from external shocks.”

Think of foreign reserves as a savings account for a country. They serve as a cornerstone of Botswana’s economic stability by providing a cushion against external shocks and fluctuations. They bolster confidence in the national currency, the Botswana pula (BWP), and facilitate smooth trade and investment transactions, thereby fostering sustained economic growth. To explain this in more simple terms:

When Botswana sells a lot of its resources, it gets more money in foreign reserves. This makes the country’s money stronger, so things aren’t too expensive for people.

If Botswana imports more than it exports (buys more from other countries than it sells), it uses foreign reserves to pay for the difference. This helps keep prices stable and ensures everyone can buy the things they need.

Foreign reserves also help when the economy isn’t doing well. For example, if there’s a global economic crisis, Botswana can use its reserves to keep the economy going and make sure people have jobs.

How Foreign Reserves Help the Economy and Ordinary Motswana

“Investing in foreign reserves is investing in the future stability of our economy.”

When a country maintains adequate foreign reserves:

They act as a financial buffer, helping stabilize the prices of essential goods like food and clothing, which ensures affordability for citizens.

They contribute to a stable financial environment, allowing banks to offer loans at reasonable interest rates, thereby facilitating access to credit for individuals looking to purchase homes or start businesses.

They provide the government with funds for strategic investments in critical infrastructure such as schools and hospitals, improving overall quality of life for citizens.

Challenges and Considerations in Managing Foreign Reserves

“Foreign reserves are the backbone of a nation’s economic resilience.”

Despite their importance, managing foreign reserves poses challenges, including the risk of depletion, balancing short-term needs with long-term objectives, and ensuring transparency and accountability in their management. Botswana must navigate these challenges with prudence and foresight to safeguard its economic stability and prosperity.

“A robust reserve of foreign currency ensures stability in times of economic turbulence.”

Foreign reserves are like a safety blanket for our economy. They help keep the country stable and growing, even when times are tough. By saving and managing its foreign reserves wisely, Botswana can continue to thrive and provide a better future for its people.

“Education is no longer confined to the four walls of a classroom; it’s accessible to anyone, anywhere.”

As an advocate for continuous learning and career development, I often encounter a common question: “Are short online courses worth it?“. In today’s rapidly changing job market, this query reflects the uncertainty many individuals face when considering their professional growth. Let’s delve into the realm of online learning platforms, including Udemy, Alison, Coursera, edX, LinkedIn Learning, Skillshare, Pluralsight, Khan Academy, and Codecademy, to shed light on the value these courses bring to career advancement.

“Flexibility and accessibility redefine how we learn, breaking down barriers and opening doors to education for all.”

Flexibility and Accessibility Online learning platforms offer unparalleled flexibility, allowing individuals to learn at their own pace and convenience. Whether it’s Udemy’s on-demand courses or Skillshare’s bite-sized lessons, learners can fit education into their busy schedules without disrupting their current commitments. This accessibility makes career development more attainable for working professionals seeking to upskill or reskill.

“Accessing relevant and specialized content ensures that learning meets the demands of today’s ever-evolving job market.”

Relevant and Specialized Content The breadth of courses available on these platforms ensures that individuals can find content tailored to their specific interests and career goals. From technical skills like coding to soft skills such as leadership, these platforms offer courses developed by industry experts and academic institutions, addressing the evolving demands of the job market. By acquiring relevant and specialized skills, learners can enhance their professional profiles and stand out to prospective employers.

“Initiative and commitment shine through as learners actively pursue knowledge, showcasing their dedication to personal and professional growth.”

Demonstrated Initiative and Commitment Completing short online courses requires initiative and commitment, qualities highly valued by employers. Whether individuals earn certificates from Udemy or badges from Khan Academy, these credentials serve as tangible evidence of their dedication to self-improvement and skill development. Employers appreciate candidates who take the initiative to invest in their own growth, showcasing a proactive approach to learning and professional development.

“Versatility and adaptability become second nature as learners embrace new skills and knowledge, ready to thrive in any environment.”

Versatility and Adaptability In an era of rapid technological advancements and industry disruptions, versatility and adaptability are essential for career success. Platforms dedicated to online learning empower learners to acquire new skills and stay ahead of industry trends. By mastering emerging technologies or exploring new fields, individuals can position themselves as adaptable assets in the job market, ready to thrive in diverse roles and environments.

“As individuals acquire new skills, their credibility grows, opening doors to recognition and career advancement.”

Credibility and Recognition While the value of traditional degrees remains undisputed, online credentials from reputable platforms are gaining recognition among employers. Certificates earned from Coursera or edX carry weight in the eyes of recruiters, signaling proficiency in specific skills or domains. Additionally, many courses offer opportunities for hands-on projects or real-world applications, further enhancing the credibility of the learning experience and its relevance to the workplace.

“Staying compliant with industry standards ensures ongoing professional relevance and growth.”

Continuing Professional Development (CPD)

Compliance for members of regulatory bodies like the Botswana Institute of Chartered Accountants (BICA) must adhere to stringent Continuing Professional Development (CPD) requirements to maintain professional competence and stay abreast of industry developments. Short online courses from platforms such as Udemy, Alison, Coursera, and others offer a convenient avenue for BICA members to accumulate CPD points while enhancing their skills and knowledge. By engaging in relevant courses, professionals demonstrate their commitment to ongoing learning and development, ensuring compliance with regulatory CPD mandates. Additionally, earning certificates from reputable online courses validates their efforts and enhances their professional credibility, positioning them as competent and knowledgeable practitioners within their field. Embracing online learning isn’t just a necessity for CPD compliance—it’s a strategic investment in maintaining professional standards and advancing one’s career within the framework of regulatory requirements.

“Education is the most powerful weapon which you can use to change the world.”

In conclusion, short online courses from these platforms are invaluable tools for career advancement in today’s digital age. By offering flexibility, relevant content, demonstrated initiative, versatility, and credibility, these courses empower individuals to take control of their professional development and unlock new opportunities for growth. While the question of whether short courses are worth may linger, the undeniable benefits they bring to career advancement speak volumes. Embracing online learning isn’t just a choice—it’s a strategic investment in one’s future success in the ever-evolving landscape of work.

“Diamonds are not just precious stones; they are the sparkling embodiment of enduring strength and timeless elegance.”

De Beers Group Auctions is a division of De Beers Group, one of the world’s leading diamond companies. The group is mostly known locally due to it’s partnership with the government of Botswana resulting in the formation of Debswana. De Beers Auctions facilitates the sale of rough diamonds through auctions to a wide range of buyers, including diamond manufacturers, traders, and retailers. These auctions provide a platform for buyers to purchase rough diamonds directly from De Beers, enabling them to acquire the stones they need for cutting, polishing, and ultimately creating finished diamond jewelry.

“A diamond is forever”

De Beers Auctions plays a significant role in the diamond industry by offering a transparent and competitive marketplace for rough diamonds. The auctions typically involve the sale of large volumes of rough diamonds sourced from De Beers’ mines and other suppliers. By participating in these auctions, buyers can access a diverse range of rough diamonds in various sizes, qualities, and grades.

“Botswana’s economy, like the diamonds it treasures, shines with resilience, fueled by innovation, diversity, and a steadfast commitment to prosperity for all.”

The decision to relocate the auction headquarters from Singapore to Botswana indicates a strategic move by De Beers to strengthen its ties with Botswana, a key player in the global diamond industry, and potentially enhance its operational efficiency and market access.

Why The Move To Botswana Is Vital

“In the embrace of something valuable, one finds solace in the proximity of true treasure.”

1. Proximity to Diamond Sources

Botswana is home to some of the world’s largest and most valuable diamond mines, including those operated by Debswana. By relocating the auction headquarters to Botswana, De Beers can be closer to the source of the rough diamonds it sells, streamlining logistics and potentially reducing transportation costs.

“Embracing local businesses isn’t just about transactions; it’s about investing in the dreams of our people, strengthening the bonds of communities, and cultivating a sustainable future rooted in shared prosperity and pride.”

2. Supporting Local Economy

Botswana has a strong commitment to local beneficiation, which involves adding value to raw materials within the country before export. By conducting diamond auctions in Botswana, De Beers can contribute to the local economy by creating jobs, supporting local businesses, and fostering skill development in the diamond industry.

“In the tapestry of governance, partnerships are the threads that weave together diverse perspectives, forging pathways to inclusive growth and sustainable development.”

3. Government Partnership

Botswana has historically maintained a stable political environment and a favorable regulatory framework for the diamond industry. By moving its auction headquarters to Botswana, De Beers can strengthen its partnership with the Botswana government, potentially leading to mutually beneficial agreements and initiatives to promote sustainable diamond mining and trading practices.

“Market access is the bridge between supply and demand, connecting producers with consumers and ideas with execution.”

4. Market Access in Africa

Botswana serves as a gateway to the African continent, which is a significant market for diamonds. By establishing a presence in Botswana, De Beers can enhance its access to African diamond traders and manufacturers, tapping into new markets and diversifying its customer base.

“Botswana’s culture Is a resilient tapestry woven with tradition, enriched by hospitality, and bound by a strong sense of community, where stories echo through time, shaping the essence of a nation.”

5. Cultural Significance:

Diamonds hold cultural significance in Botswana, where they are not only a major economic driver but also a source of national pride. By conducting diamond auctions in Botswana, De Beers can strengthen its connection to the local community and demonstrate its commitment to the country’s diamond industry and heritage.

De Beers’ decision to relocate its diamond auction headquarters to Botswana marks a significant milestone for both the company and the country. This strategic move not only underscores De Beers’ commitment to supporting local economies and fostering sustainable diamond trading practices but also highlights Botswana’s growing prominence in the global diamond industry. As De Beers and Botswana deepen their partnership, the stage is set for mutual growth and prosperity, with the potential to transform the diamond landscape in Africa and beyond.

Zimbabwe, a country known for its stunning landscapes and rich cultural heritage, is making headlines with the introduction of a new currency backed by gold. But what does this mean for everyday Zimbabweans, and why is it important?

“Gold is money. Everything else is credit.” – J. P. Morgan

Understanding the Basics Imagine you have a piggy bank where you keep your savings. Now, instead of just putting money in there, you also have a shiny piece of gold. That gold adds value and stability to your savings because even if the value of paper money fluctuates, gold tends to hold its worth over time. That’s essentially what Zimbabwe is doing with its new currency.

For many years, Zimbabwe has struggled with high inflation rates, meaning prices for goods and services go up rapidly, making it harder for people to afford the basics of life. This new gold-backed currency is a bold move by the government to try and stabilize prices and improve the economy.

“If you want to break the cycle, you have to do something you’ve never done before.”

What’s Changing? Firstly, there’s a time limit. People have 21 days to swap their old money for the new gold-backed currency. This ensures a smooth transition and helps to get everyone on board with the new system.

Secondly, the new currency, called Zim Gold (ZiG), will be backed not just by gold, but also by foreign currencies and other valuable minerals. This diversification adds layers of security to the currency, making it more resilient to economic shocks.

“Because gold is honest money it is disliked by dishonest men.”

For people in Zimbabwe and neighboring countries like Botswana, the new currency offers hope for brighter days ahead. A stable economy means more opportunities for employment, education, and healthcare, improving the quality of life for everyone. Botswana, as a neighbor, is closely watching Zimbabwe’s move. A stable currency in Zimbabwe could benefit the entire region by boosting trade and investment opportunities. This means more jobs, better infrastructure, and increased prosperity for people across borders.

While there’s excitement about the potential benefits of the new currency, there are also concerns. Some worry that there might not be enough gold and other reserves to fully back the currency, or that the value could be affected by changes in the global gold market.

“The desire of gold is not for gold. It is for the means of freedom and benefit.”

Despite the challenges, there’s hope that this new currency could be a step towards a stronger and more stable economy for Zimbabwe. By backing their money with valuable assets like gold, the country is signaling its commitment to rebuilding trust in its financial system and improving the lives of its people.

“Zimbabwe is for Zimbabweans; so are its resources.” – Robert Mugabe

Zimbabwe’s new gold-backed currency is a significant development with the potential to bring positive change to the country’s economy. While there are challenges ahead, there’s also optimism that this move will pave the way for a brighter future for all Zimbabweans.